How To Obtain a Banking License in Malta

The Banking Act of 1994 defines having a banking license in Malta as a business. The business of banking means accepting withdrawable or repayable deposits of money from the public. It also involves raising or borrowing money to lend.

Individuals and corporations looking to start a banking business in Malta will require a license. The Banking Act, Banking Directives, and the Banking Rules issued by the Malta Financial Services Authority (MFSA) mainly regulate the banks in Malta. Malta is one of the most sought-after jurisdictions when it comes to registering financial enterprises. The country offers excellent ground for individuals seeking to enter the European marketplace for banking services.

To successfully open banks in Malta, one must meet the following banking license requirements:

- Have and maintain a minimum initial share capital of €5,000,000

- Appoint at least two individuals to direct the business of the Credit Institution in Malta

- Ensure that all the shareholders and directors of the business meet the qualifying criteria

Banks must prioritise good governance and prudential banking performance. Applicants must also promote the free flow of information with the MFSA and consider depositor protection.

Setting up a bank in Malta

Malta follows a process-oriented approach when it comes to allowing individuals with banking licenses to open banks. The process is divided into three stages:

1. Preparatory Stage

The applicant, representatives and advisors shall meet with the MFSA and discuss the venture. The MFSA will then consider the application and give a preliminary indication of whether the business is possible or otherwise.

2. Pre-licensing StageThe applicant will submit the documents to the MFSA. The MFSA will review the application thoroughly before getting the business to register as a company with the Maltese Registry.

3. Post-licensing Stage

The applicant must adhere to all licensing matters before the formal commencement of business. Additionally, the business must abide by all regulations, law, and requirements issued by authorities or jurisdictions.

The license can be issued unconditionally or subject to the condition as the MFSA may deem fit.

Documents required for a banking license in Malta

- All relevant applications forms and questionnaires

- A copy of the institution’s Memorandum and Articles of Association

- Audited financial statements for the last three years (if applicable)

- A business plan, including the structure, organisation, and management systems of the prospective bank

- The identities of all directors, controllers and managers of the institution

- The identities of all shareholders with a qualifying shareholding

- The identities of the individuals who will be effectively directing the business of the prospective bank

Fees for setting up a bank in Malta

Applicants must pay a non-refundable application and processing fee of €35,000. A license fee amounts to €18,000. The annual supervision fee is 0.0002 x Deposit Liabilities, but it shall be a minimum of €25,000 and a maximum of €1,200,000.

The annual representative office fee is €3,600, paid by the representative office primarily and subsequently on the anniversary.

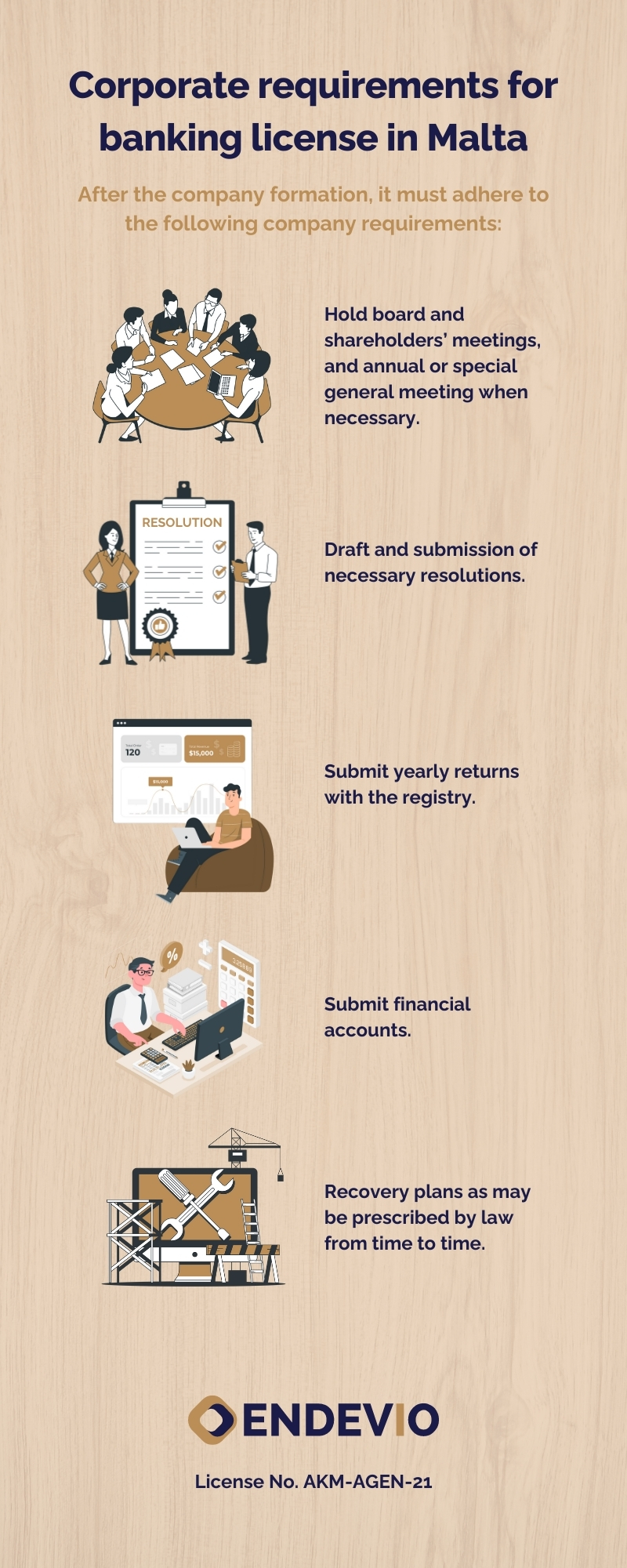

Corporate requirements for banking license in Malta

Banks could be private or public, with the latter being how the bank could obtain a listing if so desired.

After the company formation, it must adhere to the following company requirements:

- Hold board and shareholders’ meetings, annual general meetings, and a special general meeting when necessary

- Draft necessary resolutions

- Submit yearly returns with the registry

- Submit financial accounts

- Submission of resolution

- Recovery plans as may be prescribed by law from time to time

Moreover, different boards must be appointed to cater to the review and serve as supervisors under different legislative acts and regulations.

Endevio’s strategic partner, Integritas Trustees Ltd (C 22574), is authorised by the Malta Financial Services Authority (MFSA) under the Trusts & Trustees Act. Get in touch with us for more information.

Client Acceptance and KYC

The acceptance of a client is conditional and depends on ascertaining the client’s identity and the continuance of such assurance during the relationship. Identification comprises requesting a copy of a photo ID such as passport, identity card, driving license and/or a copy of their credit card or bank statement.

It is important to note that the latter examples are not exhaustive in nature. The bank will always reserve the right to ask for further information and documentation to ascertain the client’s identity.

If a client does not cooperate, the bank shall not enter any relationship with the client. This is in line with its commitment to abide by all regulations, legislation and standards appertaining to AML and KYC.

Depositor Compensation Scheme

The Depositor Compensation Scheme is a rescue fund for people deposited in failed banks licensed by the MFSA. The Scheme allows pay-out of compensations if a bank fails to meet its obligations towards depositors or has otherwise suspended payment, making the investors feel more confident and secure.

The Scheme covers deposits made with banks licensed under the Banking Act incorporated in Malta and their branches anywhere in the European Economic Area (“EEA”). It can pay the total compensation that is subject to the limit of € 100,000 per depositor.

Additionally, depositors might be entitled to receive additional compensation provided that there is evidence on specific balances held in the respective accounts.

Other obligations to abide by

All banks in Malta must be fully committed to preventing money laundering and combating the funding of terrorism for risk management and severe crime prevention. They must actively participate in international and local undertakings and initiatives regarding the said crimes.

The banks have to ensure the protection of the staff, safeguard the organisation and its reputation against the threat of criminal activities.

Money Laundering Reporting Officer (MLRO)

The banks must appoint a Money Laundering Reporting Officer (MLRO) to fulfil the following duties:

- Development of the firm’s money laundering procedures

- Have adequate identification of all clients

- Provide sufficient training for relevant personnel;

- Ensure that the firm has a clear policy when suspicion arises;

- Collate reports, consider their contents, and report suspicious to the Financial Intelligence Analysis Unit (FIAU)

- Ensure that all records are securely maintained

- Ensure that policies and procedures are maintained and effective

Ongoing monitoring process

Banks in Malta must constantly monitor the business relationship. Under normal circumstances, continuous monitoring must annually occur unless suspicion of money laundering arises or the client has a high-risk profile. Monitoring includes:

- Scrutiny of transactions undertaken throughout the relationship to ensure that the transactions are consistent with the bank’s knowledge of the client and their business and risk profile, including the source of funds and source of wealth. Information on the source of wealth and funds should be determined initially and on an ongoing basis.

- Ensure that the documents, data or information are kept up to date. In the case of companies, the bank would need to check whether there have been changes in the beneficial owners or organisational structure.

Be guided in your application for a banking license in Malta. Our team can set out an action plan and stand as your representative regarding liaising with the necessary authorities, advising bodies, and all players engaged in the licensing process.

Get in touch with us, and let us help you start your bank in Malta.